Understanding Your Net Worth At 40: A Clear Path To Financial Strength

Reaching your 40s feels like a big moment for many people, a time when you might start to think more deeply about where you stand financially. It's that point in life when you've likely had a good number of years working, perhaps managing a family, and seeing how your money choices have played out. You might be wondering, quite naturally, what a good net worth at 40 looks like, and what steps you can take to make sure you're on a solid path for the years ahead.

This period often brings a mix of excitement and, perhaps, a little bit of worry about the future. It's a common feeling, too it's almost, to look around and compare your own financial picture with others, even if you know deep down that everyone's journey is different. This article aims to give you a clear, straightforward explanation of what net worth means, why it matters at this age, and how you can work towards improving it.

Just like how keeping software updated, such as the march 27, 2025 update for Windows 11, version 24H2, brings security and cumulative reliability improvements to .NET Framework, your financial life also benefits from regular checks and refreshes. You see, Net 8.0 has been refreshed with the latest update as of June 10, 2025, and that idea of continuous improvement applies directly to your money situation. We'll explore how to approach your finances with that same commitment to ongoing strength.

Table of Contents

- What is Net Worth and Why It Matters at 40?

- Understanding Average Net Worth at 40

- Strategies to Boost Your Net Worth at 40

- Common Challenges and How to Overcome Them

- Your Financial Health Needs Regular Updates

- Frequently Asked Questions About Net Worth at 40

What is Net Worth and Why It Matters at 40?

Net worth is a simple idea, really. It's a snapshot of your financial health at a specific point in time. It shows you what you own versus what you owe. For many, this number can feel a bit scary to look at, but it's a very important figure to know, especially as you get older. It's like a financial report card that tells you how well you're doing in building long-term financial security.

The Simple Calculation

Calculating your net worth is straightforward. You add up everything you own that has value, which we call your assets. This could be things like money in your bank accounts, investments, retirement funds, your home's value, and even your car. Then, you subtract everything you owe, which are your liabilities. This includes things like your mortgage, credit card balances, student loans, or any other debts. The number you get after subtracting liabilities from assets is your net worth. It's pretty basic, actually.

So, for instance, if your assets total $300,000 and your liabilities are $100,000, your net worth is $200,000. This calculation, you know, gives you a clear picture of your financial standing. Just as the update for Microsoft .NET Framework 4.8 (KB4503548) is displayed as an installed product under programs and features, your net worth is a tangible result of your financial decisions, something you can track and monitor.

Why Your 40s Are a Key Time

Your 40s are a rather pivotal decade for your finances. By this age, you've typically settled into your career, perhaps earning more than you did in your 20s or 30s. You also have fewer working years ahead of you until retirement compared to earlier in life. This means the decisions you make now about saving, investing, and managing debt can have a very significant impact on your future comfort and security. It's a time to really step up your financial game, in a way.

Many people at 40 are balancing multiple financial demands, too. There might be mortgage payments, raising children, saving for their college, and also trying to build up retirement funds. It can feel like a lot to manage, but focusing on your net worth helps you see the bigger picture and prioritize where your money goes. It’s about building cumulative reliability improvements, much like the security updates for .NET Framework 3.5 and 4.8.1 in Windows 11 versions.

Understanding Average Net Worth at 40

When people look at average net worth figures for a specific age, it's often to see how they compare. It's human nature, really, to want to know if you're keeping pace. However, it's very important to remember that these averages are just that: averages. They can be skewed by a small number of very wealthy individuals, or they might not fully represent the diverse experiences of everyone in that age group. So, don't let them define your personal situation completely.

What the Numbers Mean

Different surveys and reports will show varying average net worth figures for people around 40. For instance, some data might suggest an average net worth for a household headed by someone aged 35-44 could be in the low to mid-six figures. But this number includes all types of households, from those with very little to those with substantial assets. It's a broad brush, you know.

It's also crucial to consider that these figures often include home equity. For many, their home is their biggest asset, and it significantly contributes to their net worth. If you own a home, your net worth will naturally look different than someone who rents, even if their savings or investment portfolios are similar. This is a common point of confusion for many, as I was saying, about understanding financial metrics.

Beyond the Averages

Instead of fixating on an average, it's much more useful to focus on your personal financial goals. What do you want your net worth to be? What kind of lifestyle do you want in retirement? These are the questions that truly matter. Your net worth at 40 should be seen as a stepping stone towards your own unique financial freedom, not a race against a statistical average. Basically, it's about progress for you.

Consider your personal circumstances: your income, where you live, your family situation, and your career path. All these factors play a big part in shaping your financial picture. A good net worth for you might be different from what's considered good for someone else. The goal, ultimately, is to ensure your financial connection is not private in a bad way, but secure and reliable for your future, unlike the `Net::ERR_CERT_COMMON_NAME_INVALID` error that warns of an unsecure connection.

Strategies to Boost Your Net Worth at 40

Building your net worth is an active process that involves several key areas. It's not something that just happens by itself. You need to be intentional about it, much like how software developers are intentional about applying updates for improved performance. Here are some actionable steps you can take to increase your financial strength in your 40s.

Review Your Assets

Start by getting a clear picture of everything you own. List all your bank accounts, investment portfolios, retirement funds (like 401ks or IRAs), real estate, and any other valuable possessions. Make sure you know exactly what each is worth. This helps you see where your wealth is currently sitting and where there might be opportunities for growth. It's like taking inventory of your financial system.

Are your assets working for you? For instance, is your savings account earning enough interest, or could that money be put into an investment that offers a better return? This kind of review is an ongoing process, too. Just as the April 25, 2025 update for Windows 11, version 24H2, includes security and cumulative reliability improvements, regularly reviewing your assets helps ensure their ongoing health and performance.

Tackle Your Debts

Reducing your liabilities is just as important as growing your assets. High-interest debts, like credit card balances, can really eat away at your financial progress. Focus on paying these down aggressively. Consider strategies like the debt snowball or debt avalanche methods to make steady progress. Eliminating debt means more of your money can go towards building wealth instead of just paying interest.

Think of it like fixing a bug in a system. The .NET Framework 4.8 update fixed an ASP.NET caching initialization bug; similarly, paying off debt fixes a drain on your finances. It improves the overall "reliability" of your financial system. You want to eliminate those "bugs" that slow down your wealth accumulation.

Increase Your Savings

If you haven't already, make saving a regular habit. Even small, consistent contributions can add up significantly over time, thanks to the power of compounding. Aim to increase the percentage of your income you save each year. Automate your savings so money moves directly from your paycheck into your savings or investment accounts. This makes it easier to stick to your plan, honestly.

Having an emergency fund is also very important. This fund should cover three to six months of living expenses. It acts as a financial safety net, preventing you from going into debt if unexpected costs arise. It's a basic, yet vital, component of financial security, like the foundational updates in .NET Framework 3.5.

Invest Wisely

For your money to truly grow, it needs to be invested. At 40, you still have a good amount of time for your investments to mature, but not so much that you can afford to delay. Consider diversifying your portfolio across different asset classes like stocks, bonds, and real estate. If you're new to investing, consider low-cost index funds or exchange-traded funds (ETFs) that offer broad market exposure.

If you're unsure where to start, consider seeking advice from a financial advisor. They can help you create an investment strategy that aligns with your goals and risk tolerance. Learning more about investing basics on our site can also be a good first step. This is a bit like seeking a simple and straightforward explanation when you're new to a complex area, such as the .NET area that someone found confusing.

Grow Your Income

Increasing your income directly impacts your ability to save and invest more. Look for opportunities to advance in your career, negotiate a higher salary, or even start a side hustle. Developing new skills or gaining certifications can also open doors to higher-paying roles. Every extra dollar you earn, you know, can be put towards boosting your net worth.

Consider how you might leverage your skills or hobbies to create additional income streams. This proactive approach to increasing your earnings is a very powerful way to accelerate your financial progress. It’s about making your financial approach high performance, much like the asynchronous and high-performance nature of the preferred approach mentioned in my text.

Common Challenges and How to Overcome Them

It's pretty common for people in their 40s to face unique financial challenges. Life often gets more complicated, and financial demands can increase. But knowing these challenges exists means you can plan for them, too.

Balancing Priorities

One of the biggest hurdles is balancing competing financial priorities. You might be saving for retirement, a child's education, a home renovation, and maybe even caring for aging parents. It can feel overwhelming, honestly. The key is to prioritize your goals and create a budget that reflects those priorities. Decide what's most important to you and allocate your funds accordingly.

This might mean making tough choices, like delaying a vacation to contribute more to your retirement fund. But these decisions, you know, are investments in your future self. It's about ensuring that your financial system is robust enough to handle various demands, just as updates ensure the stability of Windows Forms applications.

Avoiding Common Pitfalls

Another challenge is avoiding common financial mistakes. These can include taking on too much debt, making impulsive large purchases, or not having adequate insurance. These pitfalls can quickly erode your net worth. It's important to be disciplined and make informed decisions.

Stay away from get-rich-quick schemes, too. Building wealth is typically a long-term process that requires patience and consistency. Remember, there's often a "big confusion about all these" complex financial products, and you really couldn't figure out simple explanations. Stick to strategies that are straightforward and proven, even if they seem less exciting.

Your Financial Health Needs Regular Updates

Just as technology, like the .NET Framework, requires continuous updates and refreshes for security and optimal performance, your financial plan also needs regular attention. The march 27, 2025 update for Windows 11, version 24H2, includes security and cumulative reliability improvements. Similarly, reviewing your financial situation at least once a year, or whenever major life changes happen, is very important.

Life circumstances change, economic conditions shift, and your goals might evolve. Regularly checking in on your net worth, adjusting your budget, and reviewing your investments ensures your financial plan stays relevant and effective. It helps you address any "bugs" in your financial system before they become big problems. For further guidance, you might find useful information on a reputable financial planning site. It's all about proactive management, basically.

Frequently Asked Questions About Net Worth at 40

Here are some common questions people ask about their financial standing at age 40.

What is a good net worth for someone turning 40?

A "good" net worth at 40 really depends on your individual circumstances, like your income, where you live, and your personal goals. While averages exist, focusing on consistent progress and meeting your own financial targets is more important. Aiming for a positive net worth that is steadily growing each year is a very strong indicator of financial health, you know.

Is $500,000 net worth good at 40?

For many, a net worth of $500,000 at 40 would be considered a very good achievement. It indicates significant progress in wealth accumulation and likely puts you ahead of many peers. However, it's still crucial to consider your future expenses, like retirement needs and potential college costs for children, to determine if it's enough for your specific goals. It's a strong foundation, though, honestly.

How much money should you have saved by age 40?

A common guideline suggests having about three times your annual salary saved by age 40. This figure includes money in retirement accounts, investment portfolios, and savings. This benchmark helps ensure you are on track for a comfortable retirement. However, it's just a guideline, and your personal savings target might be different based on your desired retirement age and lifestyle. You can learn more about retirement planning strategies on this page.

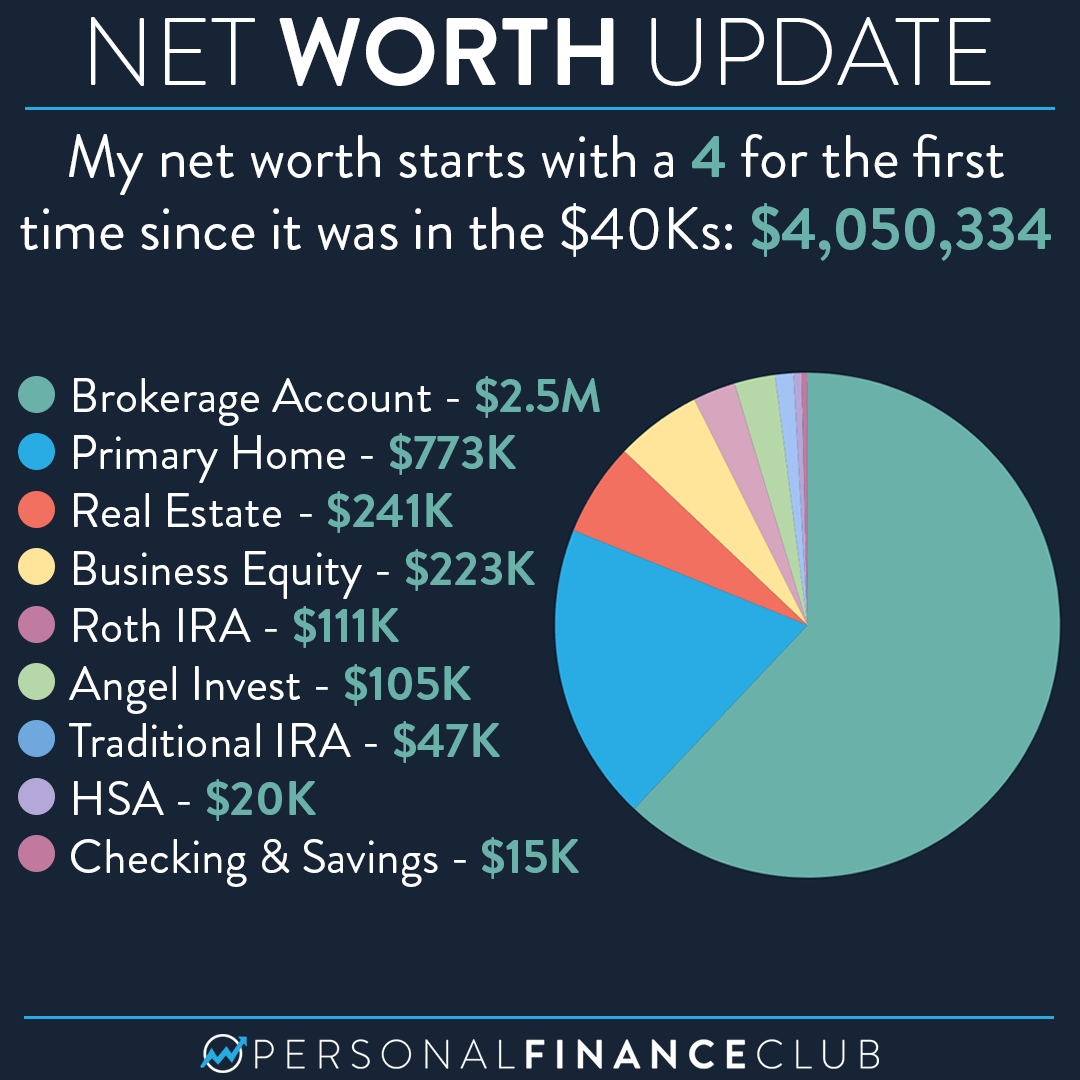

My $4 million net worth breakdown! – Personal Finance Club

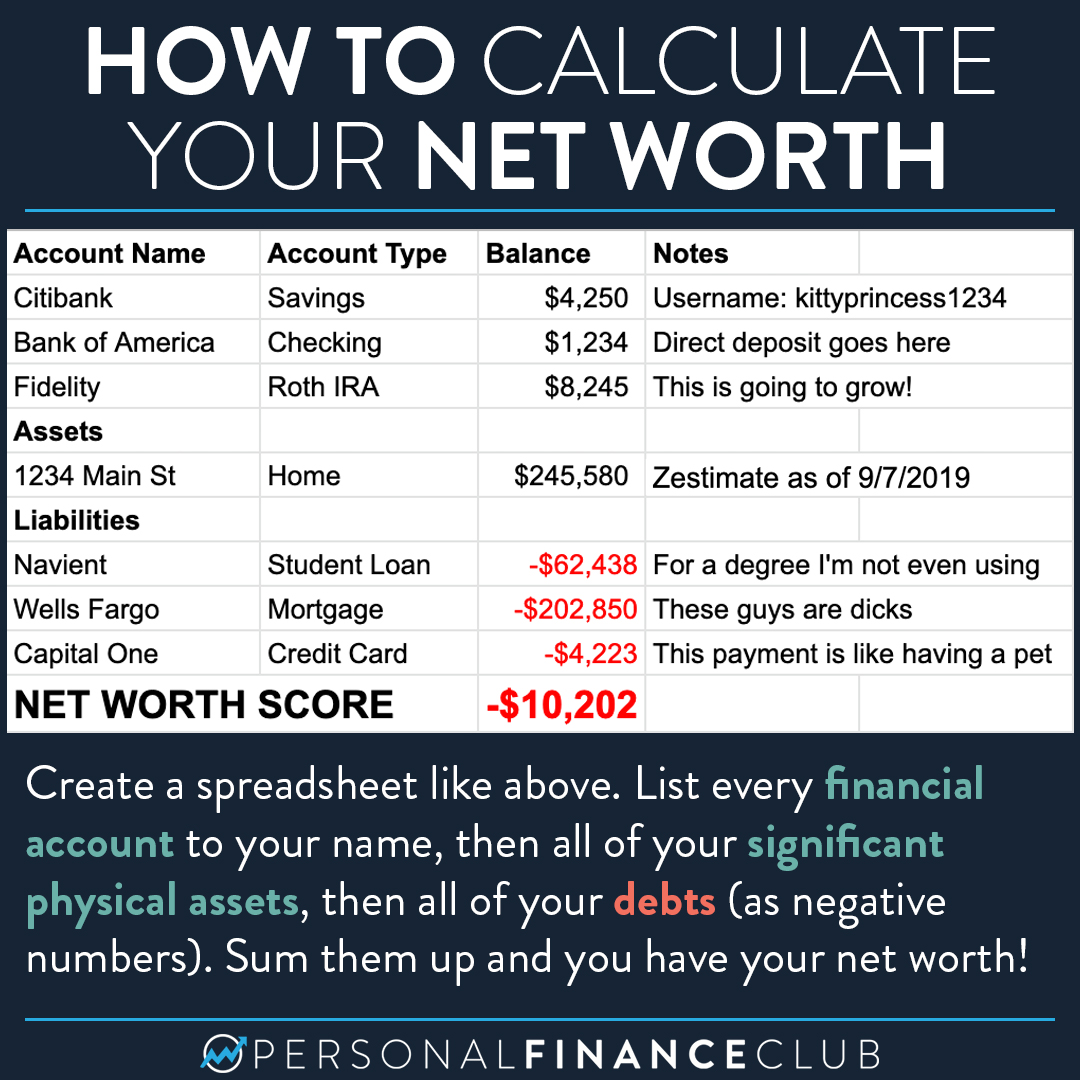

How to calculate your net worth – Personal Finance Club

NET WORTH OF A LIFE