Understanding Your **Situation Net Worth** Today: A Real Look At Your Money

Thinking about your money can feel like a big puzzle, can't it? It’s not just about how much you have in the bank, or what you owe. It is, you know, much more about where you stand right now, in your current life. This idea, often called your "situation net worth," really looks at your financial picture as it exists today, with all your unique circumstances. It is, in a way, about seeing your money in the context of your life.

When we talk about "situation," we are really talking about where things are at a certain moment. It could be, for instance, the state of events around you, or even a specific problem you are facing. My text describes "situation" as the state of things, like the present situation or how things stand right now. It is also about your own place in society, your personal state. So, when we add "net worth" to that, we are looking at your money within your current set of life circumstances. It is, in some respects, a very personal financial snapshot.

This approach is quite different from just looking at numbers on a page. It helps you see how your life, your goals, and even unexpected events, affect your money. It is, you see, a way to make your financial health feel more real and connected to who you are and what you do. This article will help you get a better grip on your financial standing, whatever your current conditions might be. We will, in a way, break it all down for you.

Table of Contents

- What is Your Situation Net Worth?

- Why Does Your Current Financial Standing Matter So Much?

- How to Figure Out Your Situation Net Worth

- Adding Up What You Own

- Listing What You Owe

- Doing the Simple Math

- Life Events and Your Financial Picture

- Starting a Family

- Changing Jobs or Careers

- Unexpected Health Events

- Buying a Home

- Retirement Planning

- Keeping an Eye on Your Financial Health

- Questions People Often Ask

- Moving Forward with Your Money

What is Your Situation Net Worth?

Your situation net worth is, simply put, the value of everything you own minus everything you owe, but viewed through the lens of your current life. My text tells us that "situation" means the state of things, how things stand, or even your social standing. So, it is not just a number. It is that number tied directly to your current experiences, your immediate surroundings, and your personal condition. This means, for example, that your financial picture looks different if you are a student compared to someone who is, say, a retiree.

It is about seeing your assets and debts in the context of your present reality. Are you, for instance, in the middle of a big move? Are you, perhaps, starting a new business? These are all parts of your "situation" that directly affect your money picture. It is, kind of, a living, breathing financial report that changes as your life changes. This concept helps you think about your money in a way that is, well, more useful for your everyday decisions.

Think of it like this: if you have a lot of student loan debt, that is part of your net worth calculation. But your "situation" includes being a student, which might mean lower income now but higher earning potential later. This context is, you know, what makes your situation net worth different from just a simple calculation. It is about the "why" behind the numbers, rather than just the numbers themselves. So, it is a very important distinction to make.

Why Does Your Current Financial Standing Matter So Much?

Knowing your current financial standing is, actually, a bit like having a map. It shows you where you are right now, financially speaking. Without this map, it is pretty hard to plan where you want to go or how to get there. My text mentions that "our situation is tough enough as it is," which highlights how important it is to grasp your current state, especially when things feel challenging. This knowledge helps you make smart choices, whether you are trying to save more or pay down debt. It is, in a way, your starting point for all financial goals.

This understanding helps you behave appropriately to your situation, as my text suggests. If your current financial standing is a bit tight, you might make different spending choices than if you had a lot of extra money. It gives you a clear picture, helping you to feel more in control. This clarity can, you know, reduce a lot of stress about money. It helps you avoid those "weird situations" where you feel unsure about your money. Knowing your financial picture gives you power.

Also, it helps you prepare for what is ahead. Life, as we know, throws curveballs. An emergency situation, like a sudden job loss or a big medical bill, can really shake things up. If you have a good grasp of your current financial health, you are better equipped to handle these unexpected events. It is, basically, about being ready for whatever comes next. It lets you see if you have enough saved for those "just in case" moments. This knowledge is, in fact, incredibly valuable.

How to Figure Out Your Situation Net Worth

Figuring out your situation net worth is a pretty straightforward process, even if it feels a bit big at first. It involves two main steps: listing everything you own and then listing everything you owe. My text talks about "the situation as follows," and that is exactly what we are doing here: laying out your financial facts. It is, you know, a simple way to get a clear picture.

Adding Up What You Own

First, you gather all your assets. These are things you own that have value. Think about, for instance, your cash in checking and savings accounts. Include, too, any investments you have, like stocks, bonds, or retirement accounts such as a 401(k) or IRA. If you own a home, its current market value counts. Any other big possessions, like a car, if it has significant value, should be included. This is, in a way, your pile of good stuff.

- Cash in bank accounts (checking, savings)

- Investment accounts (stocks, bonds, mutual funds)

- Retirement accounts (401(k), IRA, pension)

- Real estate (home, rental properties)

- Vehicles (cars, boats, RVs)

- Valuable personal items (jewelry, art, collectibles)

Make sure to get the most current values you can. For investments, check recent statements. For your home, you might look at comparable sales in your area or use an online estimator. It is, you know, about getting an accurate snapshot for your current situation. This step helps you see all the places your money is stored or tied up.

Listing What You Owe

Next, you list all your liabilities, which are your debts. This includes, for example, your mortgage balance. Any money you still owe on car loans or student loans goes here too. Credit card balances are a big one for many people. Personal loans or any other money you borrowed also count. This is, basically, your list of financial obligations.

- Mortgage balance

- Student loan debt

- Car loans

- Credit card balances

- Personal loans

- Any other outstanding debts

Gathering statements for all these will give you the exact amounts. It is, you know, important to be thorough here. Sometimes, people forget about smaller debts, but every bit adds up. This part of the exercise can be a bit sobering, but it is a necessary step to truly comprehend the situation, as my text puts it.

Doing the Simple Math

Once you have both lists, the math is pretty simple. You take your total assets and subtract your total liabilities. The number you get is your net worth. So, if your assets are $100,000 and your liabilities are $50,000, your net worth is $50,000. It is, literally, that straightforward.

Assets - Liabilities = Net Worth

This number is your financial standing right now, in your present situation. It gives you a very clear, basic picture. This figure, you know, changes over time as your assets grow or shrink, and as your debts change. It is not a fixed thing, but a moving target, so checking it regularly is a pretty good idea.

Life Events and Your Financial Picture

Your financial picture, your situation net worth, is never static. It is constantly affected by what happens in your life. My text talks about "depending on the situation," and this is especially true for your money. Major life events can, you know, shift your numbers quite a bit, for better or for worse. It is important to see how these big moments play into your overall financial health.

Starting a Family

Having children or expanding your family brings with it new expenses, for sure. There are costs for childcare, food, clothes, and eventually education. While these are wonderful additions to your life, they will likely affect your monthly budget and, potentially, your ability to save or pay down debt. This is, in a way, a major shift in your financial obligations. You might, for example, see your savings grow slower, or your expenses go up. It is a very common situation.

Changing Jobs or Careers

A new job, especially one with a different salary or benefits, can really change your financial standing. A higher salary might mean more money for savings or debt repayment. A career change, on the other hand, might mean a temporary pay cut while you gain new skills. This kind of situation can, you know, affect your cash flow and how quickly you build up your assets. It is a big factor in your current financial health.

Unexpected Health Events

Health issues, unfortunately, can come up without warning. Medical bills, even with good insurance, can be substantial. Time off work might also mean less income. These situations can, in a way, put a real strain on your finances and might lead to using savings or taking on debt. It is, basically, one of those emergency situations that can really test your financial readiness. Having an emergency fund is, actually, a very smart move for this reason.

Buying a Home

Becoming a homeowner is a big step for many people. It means taking on a mortgage, which is a significant liability. However, the home itself is an asset that can grow in value over time. So, while your debt goes up, your assets also increase. This is, you know, a complex situation where both sides of your net worth equation change. It is a very common goal, but it certainly changes your financial picture.

Retirement Planning

As you get older, your focus often shifts more towards retirement. This means saving more in specific accounts and perhaps reducing your debt load. Your income might change as you near retirement, and then again once you stop working. This is, in a way, a long-term situation that requires consistent attention to your net worth. It is, basically, about building up that asset side of the equation so you can live comfortably later on.

Keeping an Eye on Your Financial Health

Checking your financial health regularly is, actually, a very good habit. It is like getting a check-up for your body, but for your money. My text talks about "current situation" and "as things stand," which highlights the need for ongoing awareness. You do not have to do it every day, but perhaps once a quarter or once a year. This helps you see how your money is growing, or where it might need a bit of attention. It is, you know, about staying informed.

When you keep track, you can spot trends. Are your assets growing steadily? Are your debts going down? If you see things moving in a direction you do not like, you can make changes. For example, if your credit card debt is creeping up, you can adjust your spending. This is, basically, about being proactive instead of reactive. It helps you behave appropriately to your situation, as my text suggests.

Many tools can help you with this. There are, for instance, free apps and websites that link to your bank accounts and investments to give you an overview. You can also use a simple spreadsheet. The method does not matter as much as the act of doing it. The goal is to comprehend the situation, as my text puts it, and use that knowledge to make good choices for your money. It is, after all, your financial future.

Questions People Often Ask

People often have questions about their money and their financial standing. It is, you know, a pretty common thing. Here are some common questions and simple answers to help you get a better grasp of your own financial picture.

What if my net worth is negative? Is that bad?

Having a negative net worth means you owe more than you own. This is, actually, quite common for younger people, especially those with student loans or new mortgages. It is not necessarily "bad" if you have a plan to increase your assets and reduce your debts over time. It is, in a way, just your current situation. The important thing is to have a path forward, you see.

How often should I calculate my net worth?

Most people find that checking their net worth once a year is a good rhythm. Some prefer quarterly updates, especially if they are working on big financial goals. The key is to do it consistently enough to see trends but not so often that it becomes a chore. It is, basically, about finding a frequency that works for you. You want to keep an eye on your current situation without obsessing over it.

Does my net worth include my salary?

No, your net worth does not include your salary. Your salary is your income, which is how much money you earn. Net worth is a snapshot of what you own and what you owe at a specific point in time. Your salary, however, affects your net worth over time because it is the money you use to buy assets or pay down debts. So, it is, in a way, related but not directly part of the calculation itself.

Moving Forward with Your Money

Understanding your situation net worth is, you know, a powerful step towards feeling more secure about your money. It helps you see where you are right now, in your present situation, and how your life events shape your financial picture. My text reminds us that grasping the current situation is key, and that certainly applies to your money. This clarity helps you make choices that fit your life, whatever it looks like today. It is, basically, about being honest with yourself about your finances.

As you keep an eye on your financial health, you will start to see patterns and opportunities. You might find ways to save a little more, or perhaps pay down a bit more debt. Every small step can, you know, make a difference over time. Remember, your financial standing is a reflection of your life, and it changes as you do. For more insights on personal money matters, you can explore resources from places like Investor.gov, which offers helpful information.

Keep in mind that your financial picture is unique to you. There is no one-size-fits-all answer, but knowing your numbers and your current circumstances gives you a solid foundation. You can learn more about managing your money on our site, and also find out how to plan for your financial future. Taking control of your money starts with knowing where you stand, so keep learning and growing your financial knowledge. It is, after all, a very important part of your overall well-being.

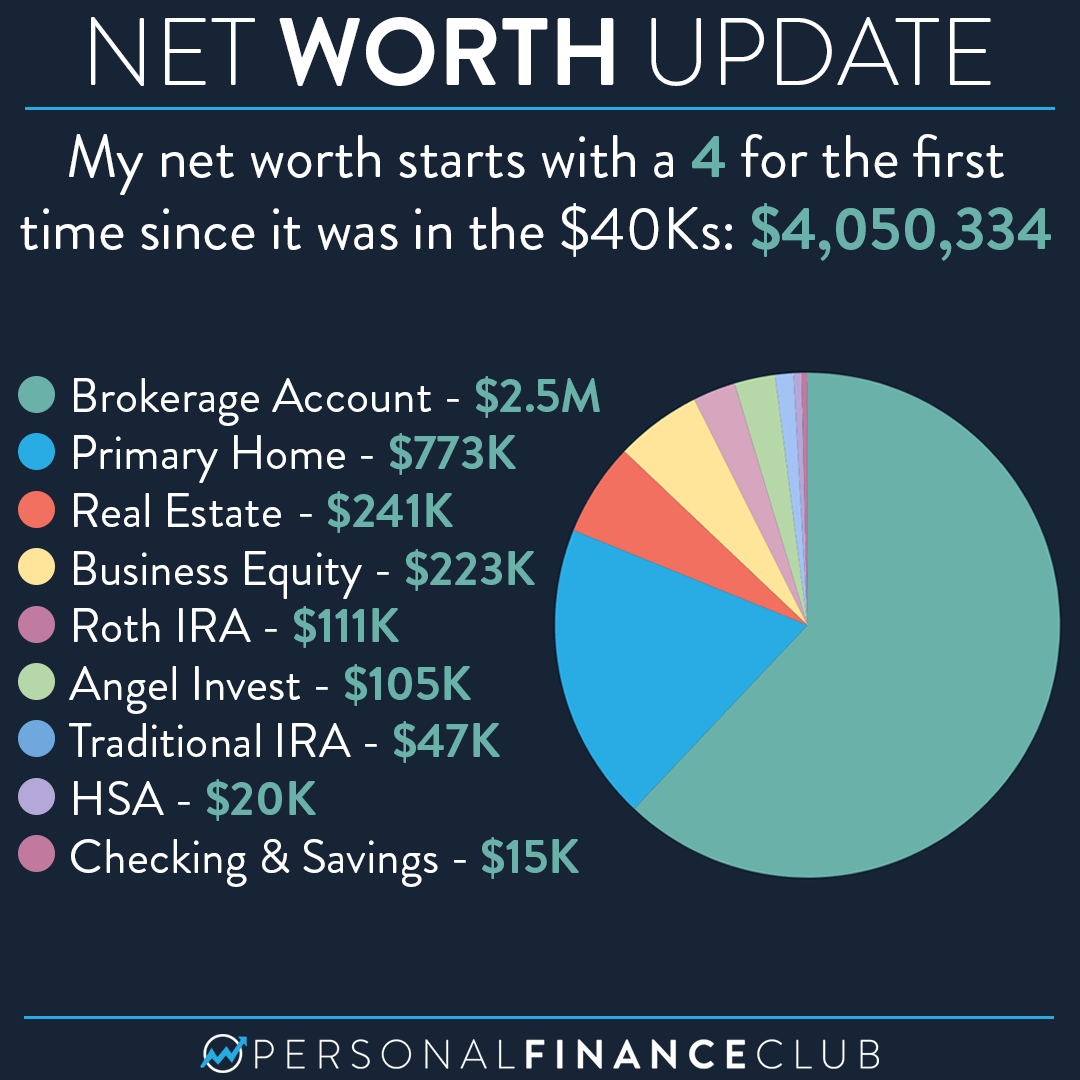

My $4 million net worth breakdown! – Personal Finance Club

NET WORTH OF A LIFE

Mike The Situation Sorrentino Net Worth - Net Worth Post